Why invest?

In my other post, “How I got over my fear of investing,” I talk about why I was so convinced investing is the key to my financial future.

You can check out the post to see the magic of investing and how it can make a difference for you too.

And now in this post, I go further into how I started my investing journey. I also share what I invest in, and outline how you can start too.

Here’s how I started investing with little money

The beginning of my investing was so unglamorous. No picking stocks, no cryptocurrency, no buying and selling real estate.

It started with just a good ole’ 401k and a boring target date fund.

Honestly though, some people forget or don’t even realize that 401k is an investment account. But there are several reasons why 401k is not only the easiest way to start investing, but also one of the most important investing accounts:

– With 401k, your taxable income is reduced (less in Uncle Sam’s pockets, more in your retirement pockets)

– Oftentimes, your employer will match a certain % of your contribution, aka you get free money

– Your contributions are automatically taken out before your paycheck so you won’t even need to think about it

As soon as I became eligible to contribute to my company’s 401k, I signed up. Maxing out my 401k was not an option for my then $47k salary, so I started by contributing just 5% of my salary.

I picked an amount I was comfortable with because I knew I could always change it later. The only thing I cared about at the time was ensuring I was getting my employer’s 401k match!

Once I became comfortable with my initial contributions (which were honestly negligible at the time), I increased my contribution percentage. I raised it by 1% little by little until I reached around 10% (I’m currently at 12%).

Of course, the actual amount you contribute will vary based on your income, but I got into a habit of raising my contributions until the maximum yearly limit.

After choosing my contribution amount, I invested. For every 401k I had with my employers- I always chose a target date fund out of the available funds in my 401k account.

A target date fund is made up of different investments and is automatically adjusted based on my target retirement age. So if your planned retirement year is 2060, you would select a fund that has the year “2060” in its name.

This simple, unglamorous step was the start of my investing journey.

Investing after 401k

After I got the hang of 401k and started increasing my contribution limits, I moved on to a Roth IRA, which is another investment account for retirement.

I know, very exciting.

This move probably sounds similar to the “Drink more water” advice from your doctor- uninteresting and slow to show results. But like drinking water, investing in a Roth IRA is a long-term game.

A Roth IRA also comes with tax advantages, except it’s advantageous when you retire. You will have to use your post-tax money to invest, but when you withdraw the money at retirement, you will not get taxed.

If you see the graph from my other post, you can see how much you would have by 65 if you invested in a Roth IRA at age 25. The $1.2 million+ you would have in your account is yours- tax-free!

The wealthier someone becomes, the more they’re concerned about taxes. Of course I want to make sure I’m not losing my money in taxes as a millionaire.

So I opened a Roth IRA through Fidelity and have been maxing it out since. Because it’s such a sweet deal, a Roth IRA has a yearly contribution limit ($7,000 for those under 50 in 2024). It also comes with an income limit, but it uses the modified adjusted gross income (MAGI) which is the income after many factors like retirement contributions, student loan interest, etc.

This means you shouldn’t count yourself out just because your income is right at the limit!

I will have a whole separate post on a Roth IRA soon. But the TLDR is- it works the same way as how you’d transfer money online to a savings account, except you have to invest the money you transfer.

So instead of leaving your money in a Roth IRA as you would in a checking or a savings account, you would log into your account and invest. What this entails is “buying” and “selling” assets, which can be individual stocks, ETFs, bonds, index funds, etc.

When I first opened my Roth IRA, I went a little overboard. But now I like to keep it simple with a diversified yet pretty aggressive portfolio. I invest mostly in Fidelity’s S&P 500 index fund (FXAIX) and smaller portions in other assets. Again, more on this in another post!

How I invest outside of retirement accounts

Once my 65-year-old self from the future was taken care of, I wanted to apply the magic of compound interest for my younger self.

I opened two accounts to invest for my more foreseeable future so that not all of my wealth was tied to my retirement:

1) The first was an individual brokerage account through Fidelity, which allows me to buy and sell different investments. I have a couple of individual stocks, but most of my money is in index funds.

2) The second account I opened was through Webull, an online stock trading platform, that I mainly used to play around with cryptocurrency. I invested very little money here, and it’s the smallest portion of my investment portfolio.

Even though these accounts aren’t tied to retirement, I plan to hold my investments in them for a long time. It’s nice to know my money won’t lose value to inflation, and over the years, it will gain interest.

The important thing to note about non-retirement accounts though is- taxes. When I do sell the investments in these accounts, I will have to pay taxes on the gains I’ve made.

So I highly recommend prioritizing your retirement investments to get maximum tax advantages before opening up individual brokerage accounts.

But what if I lose money? (My own example)

I know what you might be thinking- “OK investing sounds good in theory, but won’t I lose money?”

The short answer is- yes, but likely no if you play it wisely.

Technically, when you invest, there’s always some risk of losing money. Especially when you invest in individual stocks (aka you hold a tiny fraction of the company’s ownership), you will ride the ups and downs of the market. That’s why I don’t put all my money into individual companies.

Instead, I invest most of my money in “safer” options like low-cost index funds and ETFs (ex. FXAIX).

Think of index funds and ETFs as juice blends and stocks as juice ingredients. Instead of buying each ingredient (stock)- cutting an apple, peeling a banana, squeezing an orange, and chopping up kale- you can just get a juice blend!

Sure, you won’t get a concentrated amount of each ingredient, but you will get enough of everything. Plus, it’s easy, convenient, and cheaper than buying each fruit!

If you look at market graphs, the numbers are always changing. However, since inception, index funds have shown a 7~10% annual return.

So to go back to the original question- yes, your investments will lose value sometimes, but if you hold for a long enough time (not selling them), they will very likely jump in value.

It’s best if I share my own experience:

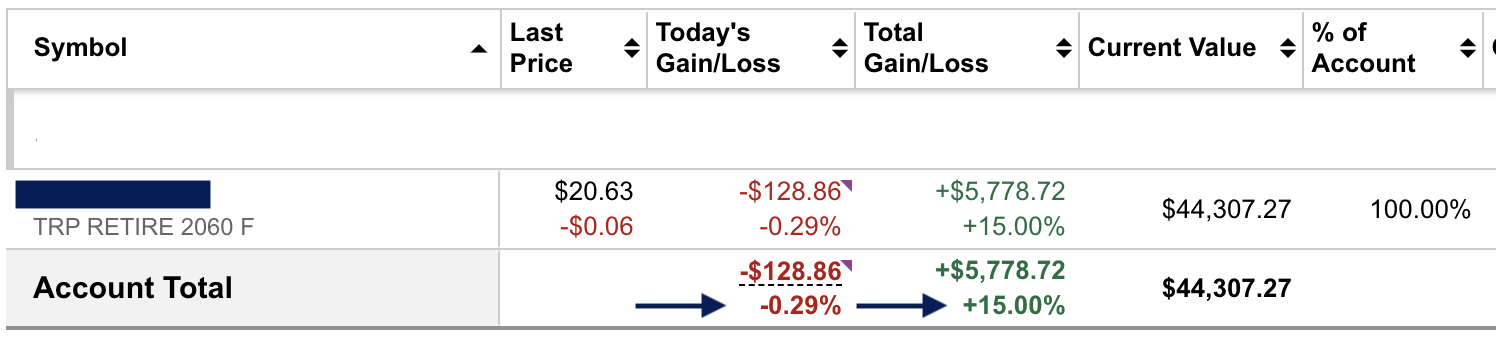

This is a real screenshot from last week of one of my 401k accounts with my past employer. Some quick observations:

– “TRP RETIRE 2060 F” is T. Rowe Price’s target date fund- a single fund that automatically adjusts my investments

– My portfolio was down 0.29% (lost $128.86 in value) on the day I took this screenshot. This is the red number in Today’s Gain/Loss

– BUT the total value of my portfolio since I opened the account 3.5 years ago went up in value by 15%. This is the green number in Total Gain/Loss

– This means the money in my account gained $5,778.72 in investments since I began contributing

This is the perfect example of how- yes, the market will fluctuate every day, but over time, your investments will likely grow.

I no longer contribute to this account because I’m at a different job, but the money continues to sit there and gain more money.

Also, the other really important thing to keep in mind is- you will lose money if you do nothing with it. Money that’s just sitting there (cash) will always lose value due to inflation.

So even if you play it “safe,” and keep your money in a locked box under your bed, you will technically “lose money” over time. So weirdly, even though investing does come with some risk, it’s also a great way to protect your money’s value.

What I’ve learned about investing

My initial contribution per paycheck was $90.38, so not life-changing, but it was pivotal for me.

It was pivotal because understanding the power of investing felt like I “cracked the code” to building wealth!

People have always mentioned investing, but I had a lot of misconceptions about it. The misconceptions included the bias I had against myself as a woman- that I didn’t make enough, know enough, or am credible enough to invest.

Starting my investing journey was also a way to challenge this notion I had. Of course I wanted to build wealth, but I also wanted to push myself to do better than what I’ve learned about money growing up. I wanted to try a road my immigrant parents and so many other women didn’t take.

I’m not going to lie- it wasn’t all fun and games. Figuring out my investment strategy also came with learning curves:

1) I had no idea what I was doing at first so figuring out my strategy took some trial and error

2) Learning about investing required a lot of research, especially for a skeptic like me

3) Investment gains were almost invisible at first. It takes a lot of consistency and time to see some real growth

But eventually, I figured it out!

Since my first 401k contributions at 23, I’ve opened a Roth IRA, a HSA, and two individual investing accounts. I’m invested in index funds, ETFs, stocks, bonds, REITs, and cryptocurrency. I continue to prioritize investing, learning about personal finance, and making money moves toward financial freedom.

And from this “journey,” I’ve learned:

1) You do not need to be rich to invest

2) You do not need a finance degree to invest

3) You do need to invest because it’s awesome (when done right)

TLDR- How you can start investing too

So you saw I started my investing journey with my first company’s 401k.

This is how I would recommend you start too. A 401k, a 403b- whatever it may be, an employer-based retirement account will be the lowest barrier to entry into the world of investing.

Then follow the steps afterward and open a Roth IRA. Unless you are making a very high income on your own or with a partner, you should absolutely have a Roth IRA.

Even as a high-income earner, you can contribute more to your 401k and HSA to bring your adjusted gross income down. Or you can do a backdoor Roth IRA!

Once you get comfortable with your retirement accounts, you will be more open to the idea of investing! Seeing how easy it can be will empower you and make you want to invest more.

Great!

You have everything it takes to seriously start forming your financial future.

Of course, you won’t see anything different in the first month. This is a long-term game. Don’t expect a lottery win here.

But if you play, you will win at this game. Just start, and keep at it no matter how boring or slow or insignificant it feels at first.

It costs to wait. So don’t wait too long to take control of your future.

If I can invest, so can you.