What do you think about when you hear the word “investing”? Do you see 25-year-old women chatting about their low-cost index funds with green smoothies in their hands?

Or do you immediately see men on Wall Street with some numbers you can’t read and some graphs that go up and down?

I can recall only two moments in my life where I actually talked about investing with a female friend. With my male friends? You know if it isn’t sports they’re talking about, it’s probably going to be about money.

Why investing seems intimidating

The Motley Fool found in their 2023 study that women’s investment account balances lag behind men’s by 44%. The same study found that women express that they feel less confident about their investing knowledge and abilities. I don’t have to look further to see evidence of this.

Many women around me have asked the same questions:

“What if I lose money?”

“Don’t you need to be rich to invest?”

“How do I start investing?”

I’m not shocked by these questions because when you haven’t tried, investing feels like one big gamble. The only way we learn about money is from our parents and their sayings like “Save for a rainy day” or “Cash is king.”. Or it’s from the movies where the guys in suits are yelling about the housing bubble and everyone becomes broke (The Big Short, anyone?).

No wonder many people, especially women, don’t feel confident about where to start with investing.

BUT (and here’s a big BUT)- when women do invest, they show better investing returns than men with differences of 0.4% to nearly 1%. That might not sound high, but 1% could be a $100k difference over time.

When I first considered investing, I also hesitated because of the prospect of losing money. I hate losing money so much that I don’t even like when friends go “You wanna bet $5?”!

But I took the small risk because investing still seemed better than losing money in cash 100% of the time and losing time because I was hesitating. And time is the biggest variable in compound interest!

What happens when you invest?

I get it. Investing can sound so daunting or intimidating, or just plain boring.

So then why are so many people doing it? Why should you?

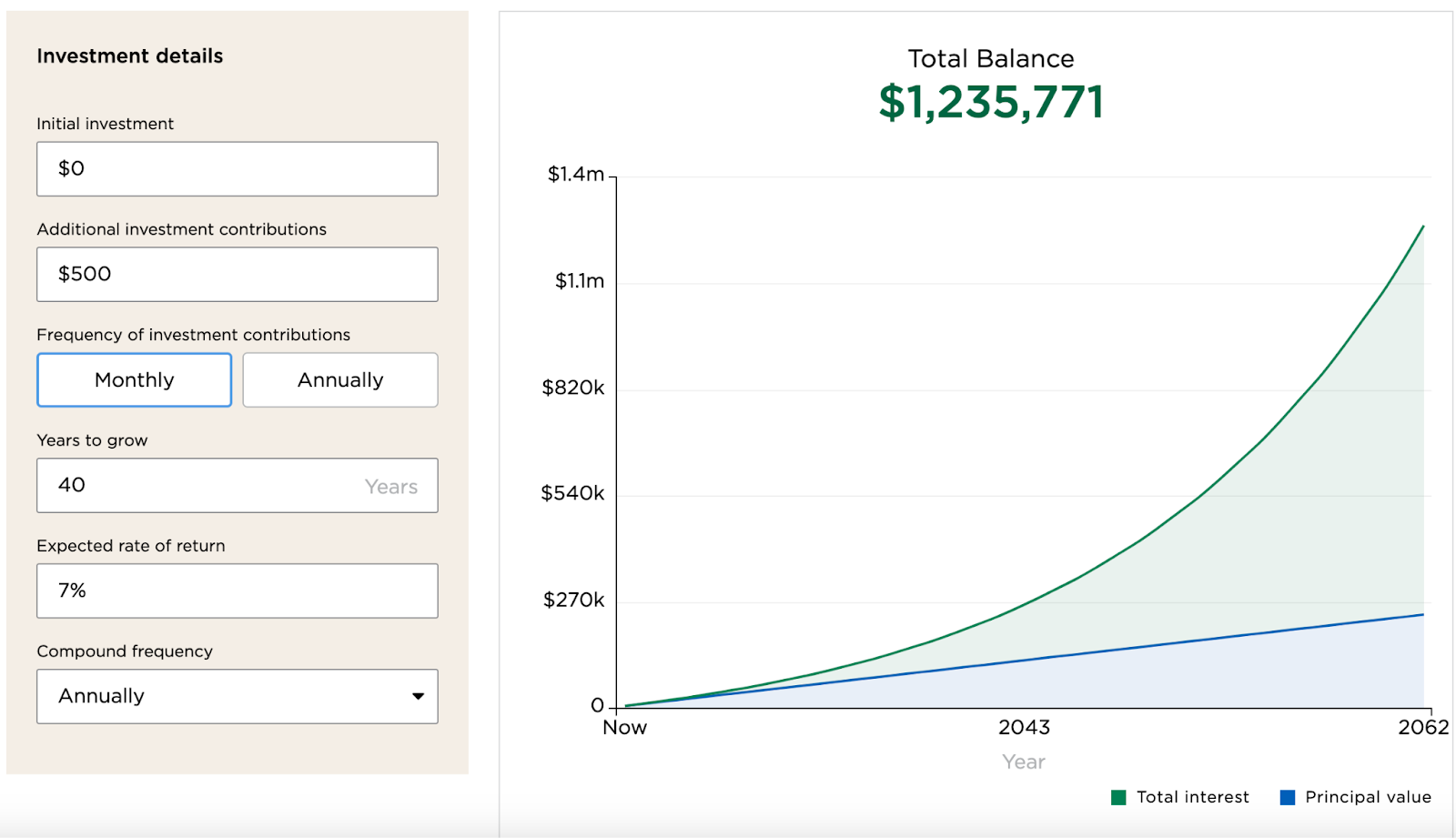

A graph is worth a thousand words in investing, so let’s start with that. Imagine you start your Roth IRA (individual retirement account) at age 25 and contribute $500 to it every month.

Look at how much your money will grow through investments in the next 40 years:

In the graph, we find out exactly what investing can do for you:

Your total Roth IRA balance will be over $1.2 million by the time you’re 65 while you only put $240,000 of your own money. That’s almost $1 million in growth just from investments!

Do you see how you don’t see that big of a return at first but there’s an exponential jump in your “total interest” around the year 2043?

The latter half of the 40 years is where most of the magic happens.

That magic is called compound interest. Yes, you learned this concept in Algebra 2. And yes, you’ve forgotten about this along with all other mathematical concepts. You don’t have to dig into your memory to figure this out though- compound interest is the interest you earn on your interest.

It’s what makes investing so powerful. Yes, in this scenario, you contribute a decent amount of your own money. But your total balance at age 65 will surpass $1 million even when you do nothing!

How do you know I will get 7% back on my investments?

Great question! I don’t.

The graph above sounds great, but there is no way to predict the market for the next 40 years. However, the only data we can reference is the past and the S&P 500 has returned an average of 11% annually over the past 50 years, which is about 7% after adjusting for inflation.

Now, if you think the world will be falling apart and the markets will all crash, you do you and hold onto your cash. But if the world was crashing, are we thinking about the stock market anyway?

Even so, the world has gone through a lot over the years and the markets still made money, so in my mind, there’s no reason for that to change any time soon.

Saving vs Investing

A common question I hear is “How is investing different from saving? Why can’t I just diligently put money into my savings?”

I’ve seen a lot of people around me over-save. Save too much- Is there such a thing?

Don’t get me wrong, saving is a great thing. But you can’t save your way to long-term wealth. Unless you were able to save $10 million, but if that’s the case, then why are you reading this blog?

Many people will make the mistake of over-saving. And I see this a lot with women. I keep bringing gender into this because this is both fascinating and alarming to me. Women can be great savers, but not many women know or talk enough about investing!

Saving is like putting your money in a locked box under your bed, except at a bank. They give you some money for the money you entrusted to them (interest), but it typically isn’t much.

Right now, the high-yield savings accounts have 4~5% interest rates, but this rate is always changing, and historically, it’s closer to 1~2%. Basically, it’ll be much less than what you’d expect from investing in the market long-term.

As you saw in the investment graph above, this is at the risk of losing potentially hundreds of thousands, if not millions of dollars over time. How? Saved money does not work for you. It’s only the starting point because you can’t invest without any money saved.

But Investing is how your money will start working for you. It’s how you can grow your wealth.

Why I started

I mean, my money making money while I’m not working? Sign me up!

When I first saw the above graph, I was sold. I put in my own numbers and saw my potential wealth shoot up. How could I not invest?

Although this concept sounds like free money (and it eventually will be), there’s still some upfront work. First, you can’t start investing with $0 so there’s that. You’ll need a job and an income.

You will also need some savings so that all your money isn’t tied up in your investments. As you saw, the real magic of investing happens with time so you don’t want your rent money invested. And of course, you’ll need essential personal finance knowledge so you can select your investments.

But after the initial legwork is done, the money you invested will literally grow by itself. It’s as simple as that.

When I first truly understood this, I felt like I cracked the code. I used to sit at my boringass first job, thinking, “How do people actually get rich?”

Even with a $100k salary (which was my income goal at the time), the math didn’t add up. I had realized Monica’s apartment in Friends was given to her from her grandmother, and Kevin’s family in Home Alone is not how average Americans live. Just working my 9 to 5 wasn’t going to get me there!

When I realized investing is how an average person becomes a wealthier person, I became dedicated to the craft.

So how did I start?

Interested in exactly how I started my investing journey? Even as a non-high-income earner?

I have a whole post that goes into detail about how I began investing with little money.

There, you’ll read about my journey- what I did step-by-step, what I’ve learned along the way, and how you can replicate this.

I highly recommend checking it out so you can also start investing.